This post is focused on educating Black and non-Black people about the causes of ethnicity wealth gaps and proposes solutions for the black community to build generational wealth. Please read with an open mind no matter your ethnicity.

Economic inequality and race are inextricably linked, and the statistics paint a stark picture of this painful truth.

For the Black community in the UK, this is a reality that cannot be ignored.

According to the ONS Wealth and Assets Survey (WAS), Black Africans and Caribbeans are worth, on a median basis, £34,300 and £85,900, only 10% and 27% of White British households respectively.

When compared to the median total wealth for a household in Great Britain of £286,600, those numbers become 12% and 30% respectively.

In addition, Resolution Foundation (RF) analysis of the ONS WAS data on financial fragility showed that 60% and 49% of Black Africans and Caribbeans households respectively, had less than £1,000 in savings compared to 28% for White British households.

These shocking statistics underscore the economic inequalities that Black people in the UK have been dealing with for generations.

It affects everything from the quality of education to career advancement, wealth creation opportunities and retirement outcomes.

So why is this the case?

What can Black people do to build wealth faster? And what examples can we look to from other ethnicities that have built wealth in the UK?

To start, it’s important to acknowledge historical issues of slavery, colonialism and institutional racism that have contributed to economic inequality.

Also, there are present-day structural inequalities in housing, employment and education that have made it harder for Black people to get access to the resources and opportunities for wealth creation.

Order our debut book, Financial Joy, a 10-week plan to help you Banish Debt, Grow Your Money and Unlock Financial Freedom.

It is written from our lived experience of achieving Financial Independence aged 34, including mortgage-free in 7 years.

Why Black People Struggle to Build Generational Wealth

Here are other contributors to the wealth disparities:

1. Immigration

Households headed by recent immigrants tend to have lower wealth outcomes because they have not had the time to accumulate wealth.

This is especially apparent when you compare the wealth of Black Africans versus people from India, who have mainly had the last 30 years to build wealth.

2. Educational Attainment and Poverty of Background

Chinese and Indians have the highest proportion of working adults educated to a degree level or higher in the UK.

Whilst 36% of Black Africans are educated at a degree level or above, this has not always translated into higher incomes.

Relative to other migrants, the Hong Kong Chinese, for example, often come from affluent backgrounds and have access to financial resources that can help them establish themselves in the UK.

They also often arrive in the UK with strong social networks that can provide them with job opportunities and other forms of support.

3. Lower Income

Whilst there has been progress in closing the ethnicity pay gaps, the gaps remain very wide.

According to DWP data, households of Indian ethnicity, for example, receive more than twice the average weekly earnings per adult for Black Caribbeans.

4. Property Ownership and Tenure

There is a strong positive correlation between property ownership and having higher wealth.

Over the last 25 years, total UK wealth has risen from 4x to 7x the level of GDP driven partly by falling interest rates, which led to capital and valuation gains in assets already held.

Indians, Pakistanis and White British people have benefitted the most with typical homeownership rates of around 70% to 80%, compared to 10% to 25% for Black Africans and 40% to 55% for Black Caribbeans according to DWP data.

In terms of wealth composition, Indians and Pakistanis have the biggest proportion of their wealth in net property, 47% and 57% respectively, compared to 33% and 38% for Black Africans and Caribbeans.

5. Sending Money “Back Home”

‘Black Tax’ refers to the financial burden that Black people in the UK (and other parts of the world) often face due to the cultural and familial expectation that they will provide financial support to their families and communities.

This support can take many forms, including paying for family members' education or helping to cover the cost of living expenses for extended family members.

Black Tax can have a significant impact on the wealth of Black people in the UK, as it can limit their ability to save and invest in their own financial futures.

It also leads to intergenerational poverty as parents can pass on the same expectations to their children, leading to a cycle of financial burden and limited wealth creation.

6. Debt Burden

Black households have a significantly higher ratio of debt to assets, leading to the cost of servicing debt often being a hindrance to building wealth.

7. Inheritance

ONS data shows that whilst White British and Indian people receive on average inheritance and gifts of £3,068 and £1,958, Black Africans and Caribbeans on average receive £1 and £778 respectively.

Inherited wealth exacerbates the wealth gap issue.

How Black People Can Build Generational Wealth

The government clearly needs to do much more to close these gaps.

But there is also plenty that Black people themselves can do to improve their financial prospects and start accumulating wealth.

1. Get Educated About Personal Finance

One of the most powerful ways of improving the financial situation of the Black community in the UK is to focus on financial education.

Every household needs to have a basic understanding of budgeting and saving as well as investing and debt management strategies.

In addition to the many resources online, there needs to be a more intentional effort on a community level to financially educate not only the adults of today but also their children.

Financial education should begin at home and we shouldn’t just wait for schools to teach us about money.

Recommended Book: Financial Joy: Banish Debt, Grow Your Money and Unlock Financial Freedom In 10 Weeks

2. Invest and Own Property

Property is important for building wealth long term.

If money is short for a deposit, people can start small and aim to pool resources with friends and family to invest in property together.

3. Lifestyle Simplification and Saving More

Adopting the mindset that wealth is mostly unseen and focusing on living a simpler lifestyle will help a lot of people live within their means and avoid lifestyles sponsored by expensive debt.

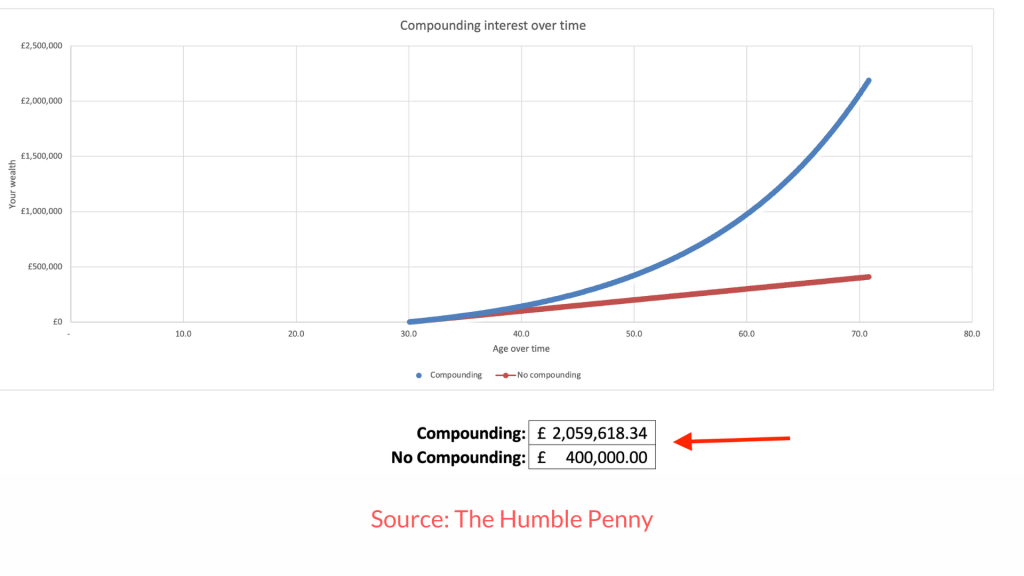

Prioritising saving and investing at least 10% to 20% per month into Stocks and Shares ISAs combined with Lifetime ISAs will help families build considerable wealth over time.

This provides some growth potential and liquidity (during times of loss of income) as Black people in the UK have the highest proportion of their wealth locked away in inaccessible pensions.

4. Create Business Opportunities to Earn More

Research by the Resolution Foundation found that all things being equal, a £1 increase in household income is associated with household wealth being £16 higher.

Entrepreneurship is a powerful tool for wealth creation, especially for Black people who have historically faced barriers in the job market.

Starting a business allows individuals to create their own opportunities and build their own wealth.

This is not without its challenges as we’ve seen with issues of access to funding for Black entrepreneurs.

Whilst we continue to work on improving funding outcomes for black entrepreneurs, we should keep learning from the examples of successful Indian and Pakistani business owners who have relied on family and community connections to secure funding and find customers.

5. Focus on Debt Freedom

With rising interest rates, debt will continue to be a big problem for families that are over-leveraged.

A big portion of disposable incomes for Black households should be focused on paying off expensive debts and where possible, overpaying on mortgages for better interest terms.

This mindset of investing in property coupled with repaying loans and not borrowing recklessly is a big part of what helped Pakistanis accumulate large property portfolios over the years.

6. Network and Collaboration

Trust is a huge issue in the black community.

There should be a focus on building long-lasting relationships with other Black people in the business world through networking events, professional organisations and mentorship opportunities.

7. Cultural Values and Community Support

Many ethnic minority communities have a strong sense of identity and culture that has helped them to build solidarity and support for one another.

Black people should look to their own cultural heritage and values as a source of strength and inspiration for building their own wealth.

Examples of such heritage and values include creativity, community, education, identity, spirituality and resilience.

The cultural heritage and values of Black people in the UK are rich and diverse, reflecting the unique experiences and contributions of people of African and Caribbean descent to British society.

Conclusion

Whilst it’s essential for policymakers to pay attention to current policies and trends in order to narrow the wealth gap, it’s also important for Black people to take practical steps to own their own stories and re-write the wealth narrative one household at a time.

Generational wealth is a possibility and our lived experience of achieving Financial Independence in our 30s even with many of the challenges highlighted, gives us hope that others can do the same too.

Order our debut book, Financial Joy, a 10-week plan to help you Banish Debt, Grow Your Money and Unlock Financial Freedom.

Financial Joy is accessible to everyone and it is available to you now, not later. Start today to create a life you love.

More posts to read on building generational wealth:

- 5 Signs You'll Become Wealthy 10 Years From Now

- If You Have £5,000 In The Bank, Do These 5 Things

- How Much Money Do I Need To Retire Comfortable?

Watch the video on version on building generational wealth:

What are your thoughts on the proposals to help the Black Community build generational wealth given current and historic challenges? We welcome thoughts and contributions from anyone of any ethnicity as a comment below.

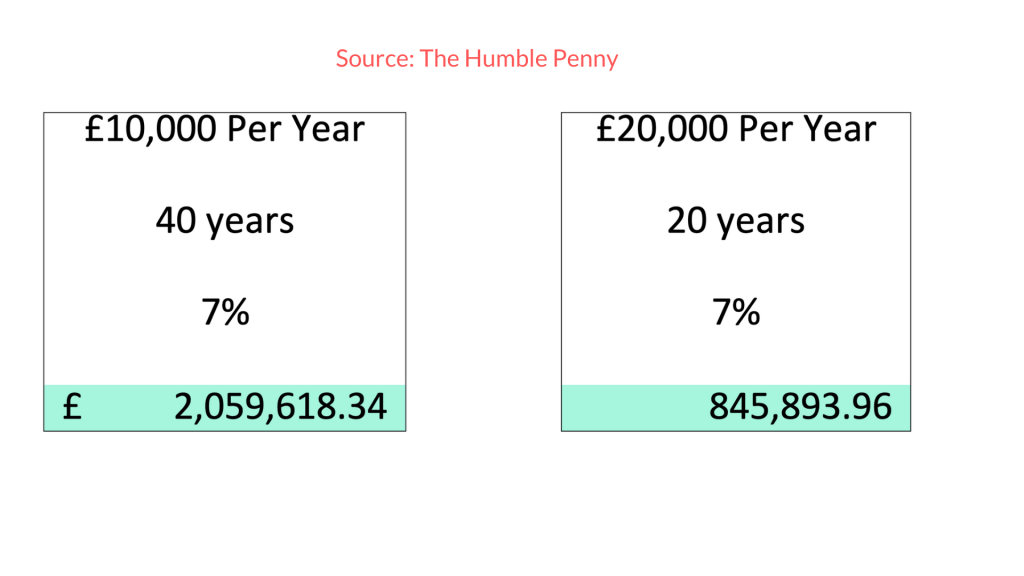

The £10k per year, over 40 years at 7% turns out to be £2,059,618.

The £10k per year, over 40 years at 7% turns out to be £2,059,618.