If you’re in your 50s and feeling unprepared for retirement, I want to start with this simple truth: it is not too late.

It may feel late and uncomfortable or even frightening when you start looking at the numbers.

But late is not the same thing as impossible.

I was asked a question by someone who said,

I’m 51 years old and don’t feel financially prepared for retirement. What should I prioritise right now?

It’s such an important question because many people are carrying this quietly. They feel really underprepared.

They’ve worked hard, life has happened, and suddenly retirement no longer feels like a distant concept. It feels close.

The good news is that retirement planning does not begin with panic. It begins with clarity.

What matters now is not beating yourself up over the past; instead, it's about taking the right steps from this point forward.

There is still time to make meaningful progress, especially if you become intentional about what retirement actually means for you and what actions you’re willing to take.

Start Planning to Retire Comfortably

If I were in this situation, here are a few steps I'd take:

🌱 Step 1: Be honest about why you are where you are

The first step is reflection, but not self-blame.

This matters because many people avoid retirement planning altogether.

They bury their heads in the sand because the topic carries shame, anxiety, regret, or uncertainty.

But if you don’t face where you are, it becomes very difficult to build a plan for where you want to go.

Ask yourself honestly:

- Why do I feel unprepared for retirement?

- What has contributed to my current financial position?

- What patterns, events, or setbacks have shaped this?

The answer might not be carelessness at all.

Perhaps you immigrated and had to start over.

Maybe you experienced divorce, health issues, a career setback, or time out of the workforce to raise children.

Perhaps your income was decent, but lifestyle creep slowly ate away at your ability to save.

Maybe you were simply surviving, and retirement was never the immediate priority.

Whatever the reason, write it down.

If you have a partner, talk about it together.

These conversations can be uncomfortable, but they create the foundation for everything that follows.

You need a clear-eyed view of your story so you can move forward with intention instead of fear.

Recommended: Before I forget to mention it, if you need tailored 121 well with your Retirement Planning, book a 121 Power Hour with me. I'll share more later.

🧭 Step 2: Define what retirement means to you personally

One of the biggest mistakes in retirement planning is assuming retirement only has one shape.

For some people, retirement means stopping work completely at 65 and spending their time relaxing, travelling, and enjoying family.

For others, retirement is not about doing nothing. It is about freedom.

Freedom to choose work they enjoy, freedom to work part-time, freedom to pursue purpose without pressure.

That distinction matters.

If your idea of retirement is unclear, your plan will be unclear too.

Think about questions like these:

- Do you want to stop working completely or reduce your hours?

- Do you want to travel?

- Do you want a quiet life close to family?

- Do you still want purpose-driven work, perhaps on your own terms?

- Do you want to remain in the same country or split your time between two places?

I recently saw an example of a couple in America who realised the traditional path was not for them.

They sold everything, retired at 55, converted an RV into a home, and chose a travel-focused life instead.

That was their version of retirement.

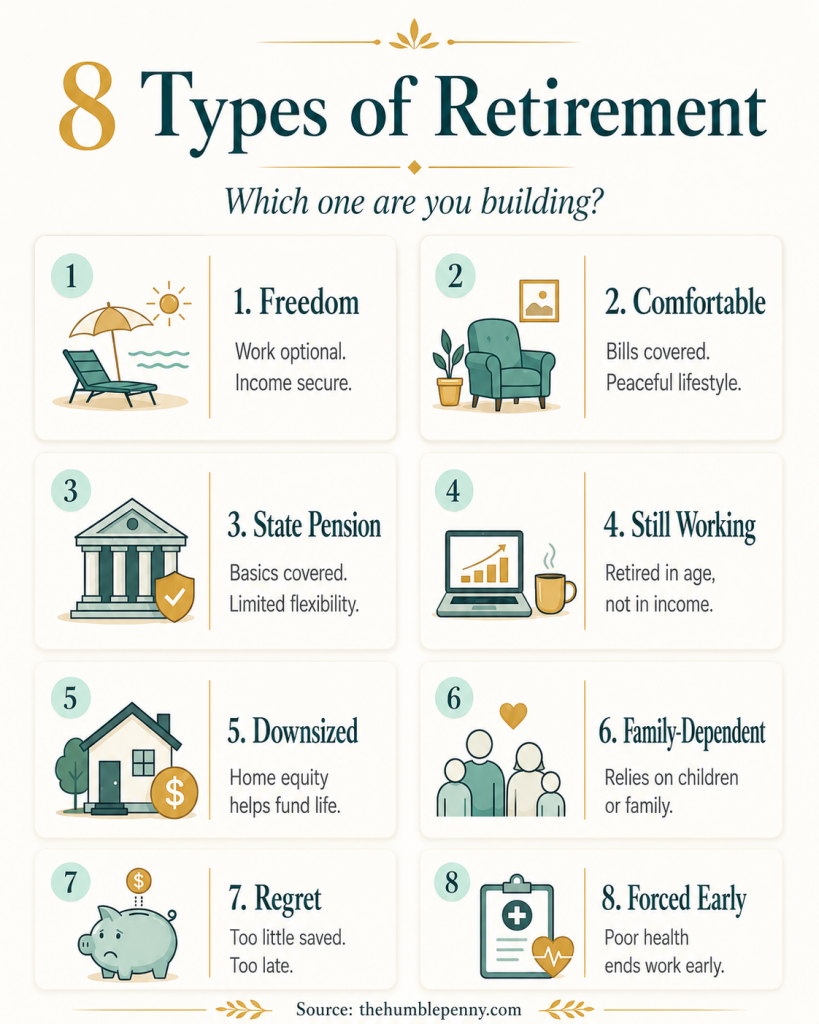

We've identified 8 types of retirement that people end up having realistically.

Which one you end up with will depend on what you do from now on.

For Mary and me, our version has always been to aim for the “freedom” type of retirement but not one that we enjoy some day.

We paid off our mortgage in seven years, invested aggressively across different assets, and worked towards a lifestyle that blends freedom, flexibility, and enjoyment now, not just later.

We often describe it as creating a life of financial joy, where you are preparing for the future without postponing all happiness until retirement.

Your retirement does not need to look like anybody else’s.

But it does need to be clear enough that you can cost it and work towards it.

Recommended: 40+ and Little Saved for Retirement?

📍 Step 3: Decide where you want to retire

Where you retire has a huge impact on how much retirement will cost.

This is one of the most overlooked parts of retirement planning.

People often jump straight to “How much money do I need?” without first asking, “Where exactly do I plan to live?” That question changes everything.

Retiring in the UK, the US, Canada, Australia, or many parts of Europe is generally far more expensive than retiring in lower-cost regions of the world.

Housing costs, food costs, healthcare, transport, and general lifestyle expenses all feed into your retirement number.

Housing is especially important.

If you are still renting in retirement, your costs may remain vulnerable to rising rents and inflation.

This is a major issue, particularly in high-cost cities such as London.

If you own your home outright, your retirement income may stretch much further.

If you plan to downsize or relocate to a cheaper area, that can change your numbers dramatically.

Also, think beyond property. Consider:

- The cost and quality of food

- Access to healthcare

- Your support network and family connections

- Climate and lifestyle preferences

- Whether your day-to-day living costs will rise or fall there

Some people choose to retire abroad because their money goes further.

Others want to stay close to family even if it costs more.

Neither option is wrong; the key is understanding the trade-off.

For us personally, good weather, lower cost of living, proximity to family/community and access to good health care options, ease of return to the UK and access to quality organic food are important.

Good food is critical for living life well, especially as we age.

This simple, affordable, and delicious meal is one I'd love to have more of in retirement. Love the variety.

🧮 Step 4: Work out how much you realistically need

Once you know what retirement looks like and where you want to live, the next step is to estimate your number.

A simple way to begin is this:

- Estimate how much you would spend each month in retirement.

- Multiply that by 12 to get your annual spending.

- Multiply that annual number by 25.

For example, if you expect to spend £2,000 per month, that is £24,000 per year.

Then:

£24,000 x 25 = £600,000

That gives you a rough retirement target, especially if you plan to retire in the US.

Another version of the same calculation is to divide your annual spending by a safe withdrawal rate. Using 4%, that would look like this:

£24,000 ÷ 0.04 = £600,000

For UK planning, a more cautious safe withdrawal rate of 3.5% rather than 4% is needed, according to research, but it would increase the amount needed.

In the above example, it would be £24,000 ÷ 0.035 = £685,714.

This is not a perfect financial planning model, but it is a useful starting point.

It gives you a tangible figure to aim for instead of a vague sense of dread.

There are, of course, many factors that affect this number:

- Whether you are mortgage-free, still have a mortgage or you rent

- Whether you are single or planning as a couple

- Whether you still support children or grandchildren

- How much travel you want to do

- What lifestyle you want in retirement

One more thing to bear in mind is the state pension.

If you are in your early 50s, the state pension may still form part of your retirement picture.

But you need to understand when you’re eligible, how much you’re likely to receive, and whether that amount will continue rising depending on where you live.

In some cases, moving abroad can affect how your state pension increases over time.

That is why location and pension planning need to be considered together, not separately.

I highly recommend reading week 9 of Financial Joy, as it goes deep into retirement planning as a starting point.

📉 Step 5: Calculate the gap

Once you know roughly how much you need, compare it to what you already have.

This is where things become very real, but also very useful.

Let’s say your target is £600,000, and currently you have £100,000 across your pension, ISAs (i.e. tax-free accounts), investments, and other retirement assets.

Your gap is £500,000.

That gap is not there to make you feel bad; instead, it is there to help you plan.

Without knowing the gap, you cannot begin to think strategically about how to close it.

For some people, the gap may be smaller because they have paid off their home.

For others, it may be larger because they are still renting or have had limited opportunity to invest.

Again, this is why honesty matters so much in step one. You need facts, not assumptions.

At this stage, pull together everything you can:

- Private pensions

- Workplace pensions

- Stocks and shares ISAs

- Savings

- Property equity

- Business assets

- Any other investments

Then compare that total against your target retirement number.

⚙️ Step 6: Decide how you’re going to fill the gap

This is the strategy stage.

Once you know your gap, you can begin building an approach around your time frame, your risk tolerance, your income, and your goals.

There is no one-size-fits-all plan here, but there are a number of paths people often combine.

These may include:

- Investing in the stock market in a disciplined, tax-efficient way

- Property investing, where appropriate

- Building or growing a business that could eventually be sold or generate income

- Downsizing to release equity from your home

- Geo-arbitrage, meaning relocating somewhere with lower living costs

- Working part-time in a semi-retired lifestyle

- Increasing income now by taking on extra work specifically to invest more

That last point is particularly important if retirement is 5 to 15 years away.

If you can generate an extra £500 (650) or £1,000 ($1,300) per month and direct that money intentionally into investments, it can make a real difference over time.

For some people, that may mean finding another job, creating a side income stream, or cutting unnecessary spending to free up more cash for investing.

The key is to stop thinking vaguely and start thinking structurally.

Ask yourself:

- What is the most realistic way for me to increase my assets?

- What can I automate?

- Which habits need to change?

- What timeline am I working with?

- Do I need expert help to build a tailored plan?

For many people in their 50s, this stage is also emotional.

There is often an urgent desire to enjoy life now, not just accumulate for later.

And rightly so.

We all know stories of people who worked and waited, only to never really enjoy the retirement they imagined. That is why retirement planning is not purely mathematical. It is also about life design.

You may choose to create a version of retirement that starts earlier, but in a lighter form.

Less work, more freedom, lower costs, and a more intentional lifestyle.

That can be just as valuable as aiming for a traditional full-stop retirement at a fixed age.

📚 Step 7: Use good resources and keep learning

You do not need to figure all of this out in one sitting, and you do not need to do it blindly.

Retirement planning becomes much less intimidating when you break it into small, manageable steps and use trusted resources to guide you.

If you prefer a DIY approach, spend time learning the fundamentals of:

- How much retirement might cost for your lifestyle

- How pensions and investing work

- How to build tax-efficient wealth

- How to estimate income from your assets

- What lifestyle changes could improve your long-term options

And if your situation is more complex, there is real value in getting personalised guidance.

A retirement plan is always stronger when it reflects your actual life, not a generic spreadsheet from the internet.

If you need tailored 121 well with your Retirement Planning, book a 121 Power Hour with me.

The most important thing is this: do not stay stuck in avoidance.

Even one focused afternoon of reflection, number-crunching, and decision-making can move you from fear to direction.

💛 Why 51 is not too late

I want to end on an encouraging note because this conversation can feel heavy.

If you are 51, or in your 50s generally, that season of life should not only be marked by financial anxiety.

It should also be recognised for what it is: a remarkable milestone.

You have lived half a century. That is something to respect.

Yes, the cost of living is high, and the world feels uncertain.

And, yes, retirement planning can seem more difficult now than it did for previous generations.

But there is another side to that story, too.

There is more access to information, more flexibility in how people live and work, more global options, and more opportunities to design life differently.

You do not need perfection from this point; you need progress and honesty about where you are, clarity about where you want to go, and courage to start taking the next step.

In my personal view, this is how comfortable intentional retirement begins, and it doesn't need to start when you're 65.

Frequently Asked Questions

Here are answers to additional frequently asked questions:

Is 51 too late to start retirement planning?

No. Starting at 51 is later than many people would like, but it is absolutely not too late.

What matters most is getting clear on your retirement goals, understanding your current financial position, and taking focused action to close the gap.

How much money do I need to retire comfortably?

A simple starting point is to estimate your annual retirement spending and multiply it by 25.

For example, if you need £24,000 per year, you might aim for around £600,000.

This is only a rough guide, and your actual number will depend on where you live, housing costs, lifestyle, and whether you expect any pension income.

Recommended guide: How Much Do I Need to Retire Comfortably?

I also recommend taking a look at the Retirement Living Standards.

What if I am far behind on retirement savings?

First, work out the gap between what you need and what you currently have.

Then create a realistic plan to close that gap through investing, increasing income, downsizing, relocating, working part-time for longer, or combining several approaches.

Feeling behind is not the same as being out of options.

Should I still invest if retirement is only 10 to 15 years away?

For many people, yes.

If retirement is still several years away, investing may still play an important role in growing your assets.

The exact approach depends on your risk tolerance, timeline, and wider finances, but many people in their 50s still use investing as part of their retirement planning strategy.

Does where I retire really make that much difference?

Yes, it can make a huge difference.

Housing, food, healthcare, transport, and taxes vary significantly by location.

A retirement that feels expensive in one country may feel very manageable in another.

This is why a lot of people move to countries in Asia and Africa, for example.

Deciding where you want to live is one of the most important retirement planning decisions you can make.

What if I do not want to stop working completely?

That is perfectly valid.

Retirement does not have to mean a complete end to work.

Many people prefer a semi-retired lifestyle with part-time work, flexible projects, or purpose-driven activity.

In fact, that approach can reduce financial pressure and make the transition into retirement much smoother. Plus, it actually keeps you alive!

Wherever you are starting from, begin there.

Reflect honestly, define your version of retirement, run the numbers, find the gap, build the plan and keep going.

Comfortable retirement is not only for people who got everything right in their 20s or 30s. It is also for people who are willing to get intentional now.

Here are more resources to help you plan for a comfortable retirement:

- Book a 121 Power Hour with me for retirement coaching with me

- Read The Wealth Habit book: Small Changes Will Make You Rich

- The Financial Joy book: Banish Debt, Grow Your Money and Unlock Financial Freedom in 10 Weeks

- Why Do You Have The Audacity to Dream Big?

- How to Make Work Optional In Every Decade of Your Life

Here is a video version of this blog post to watch and share with others who want a comfortable retirement:

As always, in all things, be thankful and seek joy.