What if I told you there are now thousands of everyday people in the UK who’ve quietly become ISA millionaires, using nothing but legal tax shelters and long-term investing?

No fancy tricks. No lottery wins. Just real people, real stats, and real wealth.

In this post, we’ll be breaking down the surprising truths behind the ISA millionaire boom and what they did differently.

We’ll reveal some compelling and unusual stats about ISA millionaires, and more importantly, we’ll give you practical steps so you can start your own journey.

If you’ve got an ISA or you’ve been sleeping on it… this could be the wake-up call you need.

Note that although today’s post is focused on ISA Millionaires and how they got there, you don’t need to be a millionaire to be or feel successful.

If you love the sound of what’s coming, please take a second to share this post with one person, as it helps to encourage more people to read our posts.

If you are new here, we run this blog as husband and wife with a small team.

We achieved Financial Independence at 34, including mortgage-free in 7 years while raising two children in the UK.

Ken: I’m a Chartered Accountant, a Financial Coach and Business Coach and a former Chief Financial Officer.

Mary: I’m an Entrepreneur and former E-business Analyst.

Together, we’re the founders of The Humble Penny and Financial Joy Academy.

Authors of our new book, The Wealth Habit, a groundbreaking, behaviour-driven approach to wealth-building that rewires the way you think about money, turning financial success into a series of tiny, effortless, repeatable actions.

And Sunday Times Bestselling Authors of Financial Joy, a 10-week Plan to help you Banish Debt, Grow Your Money and Unlock Financial Freedom.

How Ordinary People Became ISA Millionaires

Let's explore real stats, surprising truths and how to join them.

The Rise of ISA Millionaires

Did you know that the number of ISA millionaires in the UK has more than tripled in just three years?

- In 2016, there were just 570 ISA millionaires.

- In 2020, there were just over 1,000,

- In 2023, that number hit 3,180 (triple what it was in 2020),

- In 2025, over 4,850!

And it’s not just a handful of people at the top.

There are about 7,000 people with ISAs worth between £750,000 and £1 million, and a staggering 30,000 with between £500,000 and £750,000.

This certainly surprised us! Take a moment to react in the comments. Are you shocked by these stats?

We asked the Humble Penny YouTube audience how much they had in all ISAs combined (i.e. cash ISA, Lifetime ISA, Stock and Shares ISA, etc) and here is what they said:

This tells us that there are clearly other factors at play e.g. income levels, money habits/behaviours and age differences.

👉🏽Need 121 help to invest smartly in your ISA? Book a coaching session with us here.

How Long Does It Take To Become an ISA Millionaire?

According to data obtained following a freedom of information (FOI) request:

It takes them an average of 22 years to become ISA millionaires.

This tells us straight away that most ISA millionaires are older than people who typically read our posts but it’s also very encouraging to think that the average time taken to become an ISA Millionaire is 22 years!

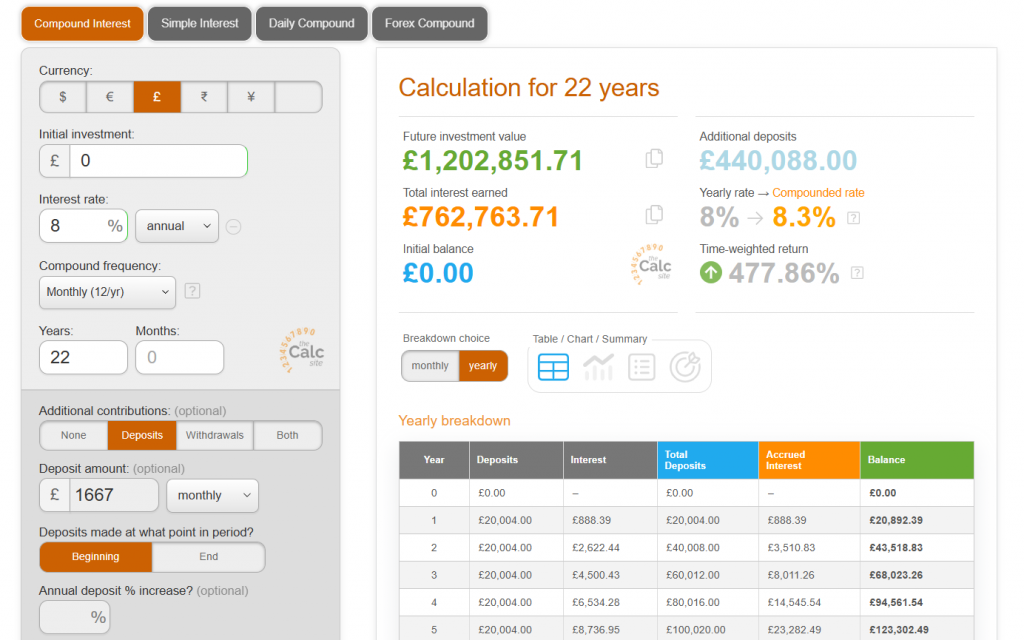

We ran a scenario on a compound interest calculator to see what average investment return is needed to achieve a £1m ISA in 22 years assuming you max out £20k a year, which is equivalent to around £1,667 per month.

Obviously, most people won’t be able to do this, but we thought it was an interesting insight to learn.

We learned that you’d need your investments to generate around an average of 8% return per year for your £20k annual investment to reach £1.2m in 22 years, even if you started with Zero today.

So someone who is aged 30, for example, would have a £1.2m portfolio by the age of 52.

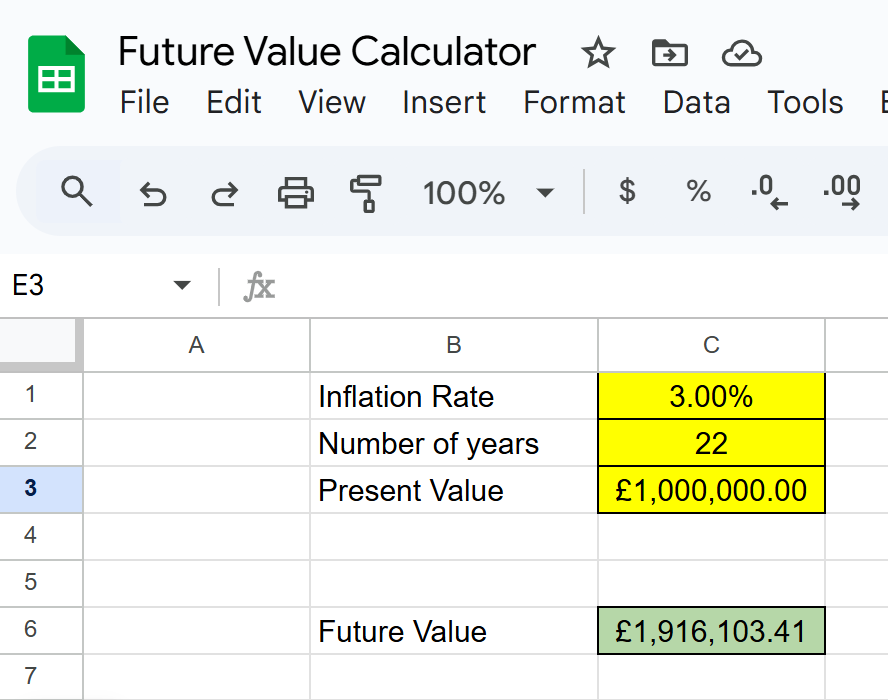

But note that due to inflation, to get the purchasing power of £1m today, you’d need around £1.9m assuming 3% inflation rate.

This implies a need to invest more or get a higher investment return on your money.

But remember, you don’t need a million pounds or dollars to feel wealthy or successful!

Who Are ISA Millionaires?

You might be picturing city bankers, but the average age of an ISA millionaire is actually 73.

And while most are older, there are a few in their 30s and even one in their 20s!

This implies that those in their 20s and 30s got lucky with investing in some individual stocks.

We definitely do not recommend waiting until the age of 73 in order to enjoy your money.

Balance is important, and this is why we wrote our book, Financial Joy, to help you stop worrying about money and start enjoying your future while being confident that you’re working towards financial independence in the years ahead of you.

We looked after our finances for years, prioritising investing, and as a result of that, it has helped to create time and financial freedoms in our lives. Please do what works for you!

The stats on ISA millionaires also show a gender gap: about 67% are men, 33% are women.

This specific data comes from Interactive Investor and could differ for other platforms.

Are you enjoying this post so far? Please take a moment to comment and share it with others.

What Makes an ISA Millionaire?

So, what’s their secret? Here are some traits and habits that set ISA millionaires apart:

- Start early: Time is their greatest ally, harnessing the power of compounding growth.

- Clear goals: Almost all ISA millionaires set a specific target and a deadline for reaching it.

- DIY investors: Most make their own investment decisions rather than relying on advisers, who, statistically, underperform the market. This also keeps fees low.

- Consistency: They contribute regularly, often increasing their amounts as their income grows.

- Long-term: They don’t worry about the short-term noise

How Do ISA Millionaires Invest?

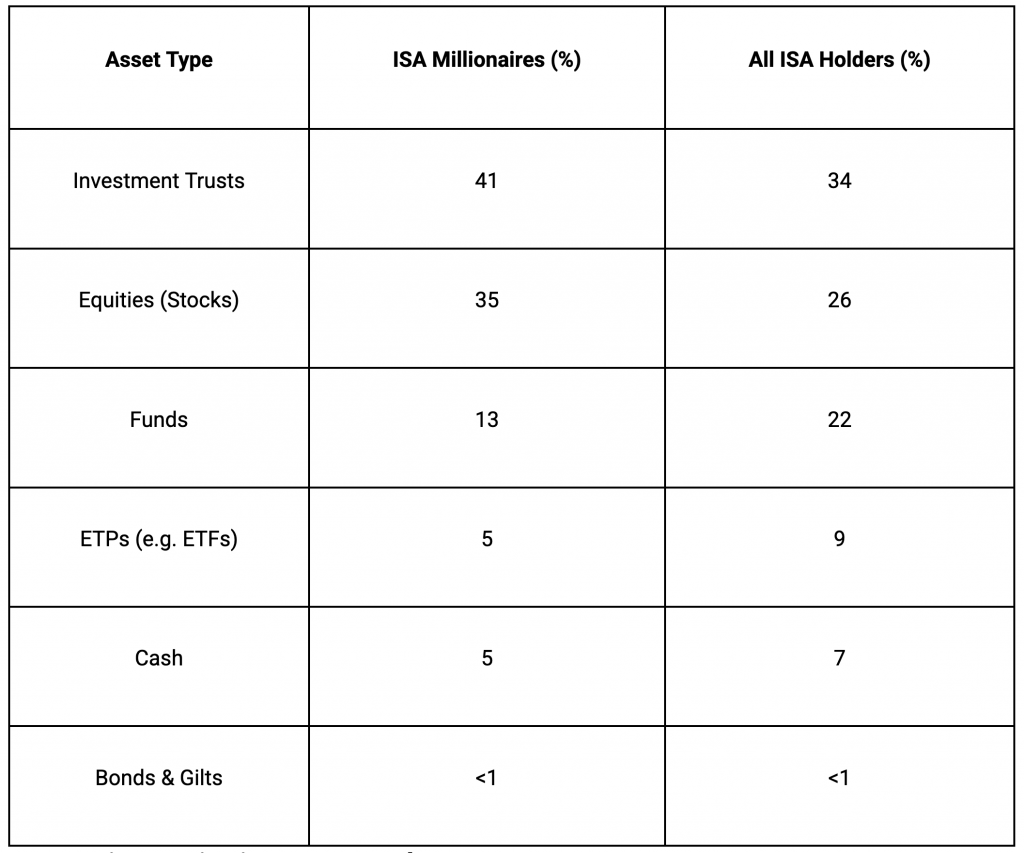

Here is some data on this from Interactive Investor:

As expected, a big proportion of their investments are in stocks, funds and ETFs.

We were really surprised by the fact that 41% of their investments were in Investment Trusts.

If you’re wondering how Investment Trusts compare to Index Funds and ETFs, below is a side-by-side comparison:

Notice also how cash is less popular among millionaires—they focus on growth assets like stocks, Index Funds/ETFs and investment trusts.

This implies that they kept around 5% in a cash ISA and the rest in a Stocks and Shares ISA.

There has been a lot of debate in the UK about cash ISAs vs Stocks and Shares ISAs.

Both have a place on the wealth-building journey.

For us, beyond keeping an emergency fund in a cash ISA, investing via Stocks and Shares ISAs and Lifetime ISAs has been a complete game changer.

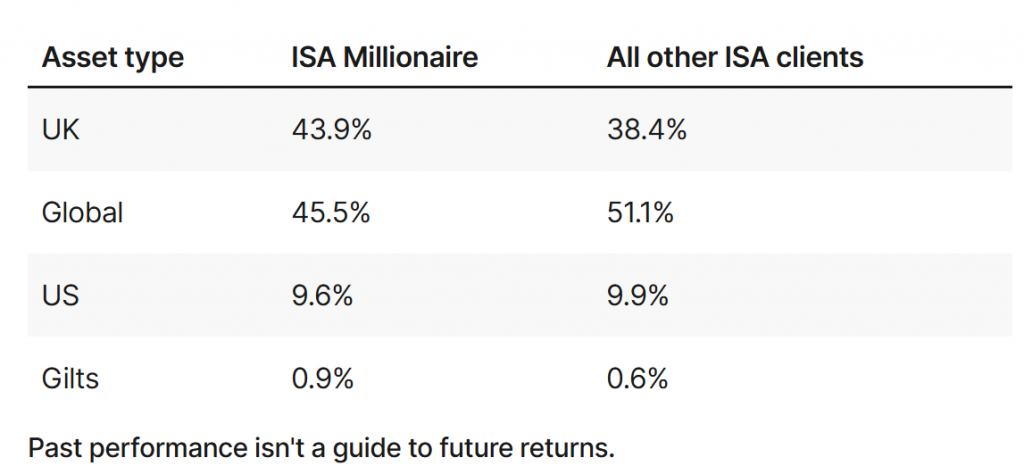

In addition to the asset classes mentioned above, we have data from Hargreaves Lansdown on how ISA Millionaires invest geographically:

Again, we were surprised to see that a large 43.9% of their investments were in the UK and only 9.6% in the US.

However, 45.5% is invested globally, and a large proportion of that will be US exposure.

This says a lot and possibly points to a generational difference.

Given the average age is 73, it’s likely these millionaires started investing in the UK when the economy was doing well and perhaps have stuck with it.

What do you guys think? Jump in the comments and let us know.

Here’s an unusual insight: 32% of ISA millionaire contributions in the last year were made in just one month—April, right after the new tax year started.

Early birds really do get the worm!

And get this: the ISA allowance has always been capped, currently at £20,000 a year, so it’s not about dumping huge sums in at once.

It’s about maximising that allowance every year, consistently.

Read: Should I Get a Stocks and Shares ISA Today?

Why Building Your ISA Is More Important Than Ever

Before we dive into the action steps, let’s talk about why building your ISA is more important than ever.

With AI and automation advancing rapidly, millions of UK jobs, especially in routine or entry-level roles (and increasingly more professional jobs) are at risk of being automated.

Even the government estimates that up to 30% of jobs could be impacted by 2030.

That means job security isn’t what it used to be, and relying on a single source of income is riskier than ever.

And it’s not just about job security.

With the UK facing structural and economic changes and increasing uncertainty, having a well-funded ISA gives you something incredibly valuable: freedom and flexibility.

If you ever decide or need to move abroad, you can keep your ISA open and continue to enjoy tax-free growth on your investments, even as a non-UK resident.

You won’t be able to add new money while living abroad, but your existing ISA stays protected from UK tax, and you can transfer it between providers if you wish.

That’s a powerful safety net.

It means you’re not tied to one country’s fortunes or policies.

Your ISA can help you take control of your financial future, wherever life might take you.

So, let’s talk about what you can do today to protect your future…

Action Steps—How You Can Start Your ISA Investing Journey

Ready to start your own journey? Here’s what you can do:

- Start now, no matter your age or income. Even small amounts, invested early, can grow significantly thanks to compounding.

- Max out your ISA allowance if you can: that’s £20,000 per year.

- Increase your contributions over time, especially after pay rises or windfalls.

- Focus on growth investments, consider stocks, investment trusts, and funds (e.g. index funds and ETFs).

- Set a clear goal. Write down your target and a deadline.

- Review your investments regularly, but don’t be tempted to overtrade.

- Educate yourself. DIY investors tend to do better, so learn the basics and take control.

If you’re serious about becoming an ISA millionaire or just want to take control of your financial future, while learning directly from us and our community of Dream Makers, we invite you to join us at Financial Joy Academy.

It’s a step-by-step membership platform we created to help motivated people like you build financial freedom faster.

You’ll instantly get to:

- Join us daily for our Lunch Time Club,

- Access ALL our practical classes,

- Follow our tailored step-by-step Success Paths,

- Get group coaching from us every 2 weeks,

- Join our supportive community of Dream Makers, and

- Get an Accountability Partner to keep you on track.

We’ve been where you are now, and FJA is designed to guide you every step of the way.

Whether you’re just starting or already investing, or you simply want to learn how to make extra money from a side hustle in tried and tested ways.

If you want to stop feeling overwhelmed and start making real progress, this is exactly what you need.

We look forward to welcoming you to our community of Dream Makers.

Conclusion

Becoming ISA millionaires is possible for us, too, and it's not too late! Start small 😀

You may have less than £20k in your ISA now; however, see this post as inspiration for what's possible.

Focus on your why for investing 📈.

For us, it's optionality and time freedom with each other and our children. What is your why?

👉🏽 If you need 121 help to invest smartly in your ISA, Book a 121 coaching session with us here.

Is becoming an ISA millionaire something you think is possible for you one day? Jump in the comments and let us know.

Don’t go anywhere, check out these next posts to help you on your investing and ISA millionaire journey:

- Read The Wealth Habit book

- Invest This in an ISA to Make £2,000 Monthly Passive Income (Tax-Free!)

- Work Smarter, Not Harder: 8 Wealth Strategies

- How to Make It In the UK (Even When It Feels Impossible)

Frequently Asked Questions

Here are some frequently asked questions.

1) What is an ISA?

An ISA stands for an “Individual Savings Account” with tax-free benefits.

There are 4 types of Individual Savings Accounts (ISA):

- cash ISA

- stocks and shares ISA

- innovative finance ISA

- Lifetime ISA

You don't pay any tax on:

- interest on cash in an ISA

- income or capital gains from investments in an ISA

If you're reading from America, the nearest US version of a UK ISA is the Roth IRA.

2) Do you know how many of the ISA millionaires had PEPs that they transferred/converted into ISAs?

Great question! We've been asked this before, and unfortunately, we don't know how many had PEPs.

3) Does the average of 22 years capture that fact? Given the annual ISA limit was much lower than £20k pa for most of the last 22 yrs, their returns far exceeded 8% per annum – that must have been down to some good/lucky stockpicking, rather than just holding passive ETFs?

It's implied that a number of them had individual stocks that did well over time.

But what we don't know is how many lost money from doing the same, and hence isn't reported in the headline numbers.

4) What are the data sources?

They come from a combination of research by various investing platforms and freedom of information requests. Here are the links:

Interactive Investor – How ISA millionaires invest

Hargreaves Lansdown – Where ISA millionaires invest

Money Week – Stats on ISA millionaire growth

Here is a full video version of this post on ISA millionaires:

Thanks again for reading, guys. And as always, in all things, be thankful and seek joy! 💛