The Real Reason Young People Are Leaving the UK

Something big is happening in the UK right now, and almost nobody is talking about it honestly.

A record number of young people are leaving the country.

Not for a gap year. Not for sunshine.

But because the maths of life in Britain… simply isn’t adding up.

Today we’re diving into why a net 110,000 under-35s left the UK in the last year — and what that means for your financial future, whether you stay or go.

And stay with me, because I’ll also share why, for some people, leaving the UK could be catastrophic, and what many people don’t realise about working abroad.

I want to be clear, I’m not writing this post to encourage you to leave the UK. No.

Today, I want to focus on what the data says and share some of my observations so that you can make a decision you won’t regret.

I want to see your reactions in the comments.

If you plan to leave the UK, comment with an aeroplane emoji ✈️, and if you plan to stay in the UK, comment with a Union Jack emoji 🇬🇧.

Please keep all comments respectful, as I know a topic like this can be divisive, so let’s pls respect everyone’s views.

My name is Ken of The Humble Penny and Financial Joy Academy, I’m a Chartered Accountant, Former Chief Financial Officer and Financial Coach.

👉🏽Together with my wife Mary, we’re Sunday Times Bestselling Authors, and we recently announced our new book, The Wealth Habit, which is all about the small changes that will make you rich.

The Wealth Habit is a groundbreaking, behaviour-driven approach to wealth-building that rewires the way you think about money, turning financial success into a series of tiny, effortless, repeatable actions.

Thank you to everyone who has ordered a copy so far! It really means a lot to us.

And good news, we agreed to an Italian translation for The Wealth Habit, and we expect more language translations the more you guys support us by ordering and gifting copies.

📍 So please order your copy of The Wealth Habit here.

Share this post with others who are interested in this topic.

Let’s dive straight in!

The Real Reason Young People Are Leaving the UK 🇬🇧

Given we have a lot to cover, we'll break it all down into different parts below.

Part 1 – What the New ONS Data Reveals

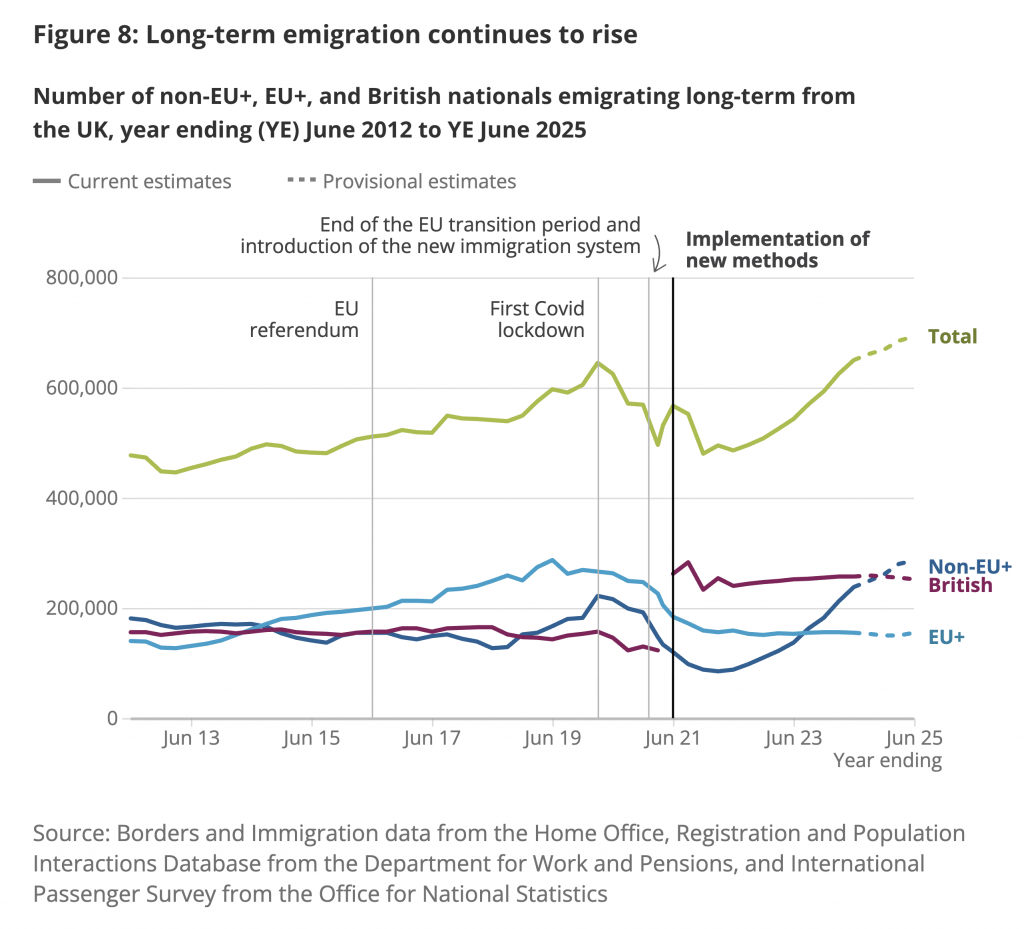

First, let’s look at an Office for National Statistics (ONS) chart of total emigration from the UK i.e. people leaving the UK to live in another country for a period of at least 12 months.

The greeline shows that the total number of people leaving the UK is the highest it has been, looking as far back as 2012.

693,000 people of different nationalities left the UK.

Above is a split by nationality.

- non-EU+ nationals (dark blue line) accounted for 41% of total emigration (286,000)

- British nationals (purple line) made up 36% (252,000)

- EU+ nationals (light blue line) made up 22% (155,000)

For Non-EU nationals leaving the UK, the top 5 are Indian, Chinese, Nigerian, Pakistani and Ukrainian. Here is a chart:

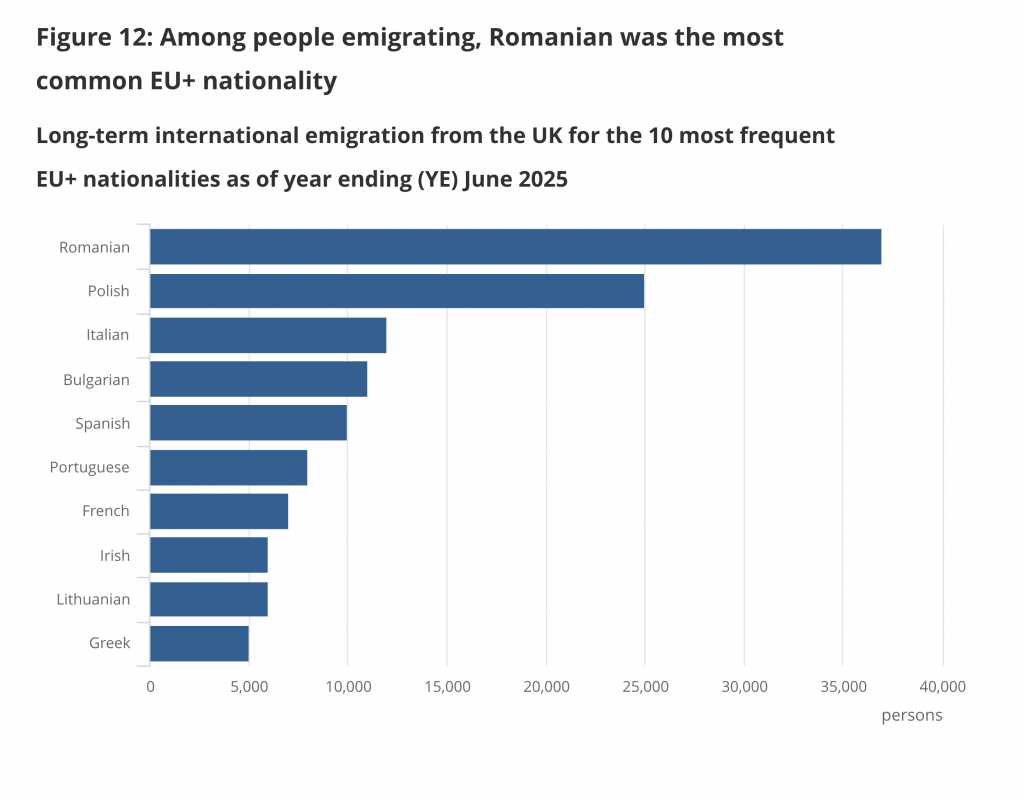

For EU citizens leaving the UK, here is a summary according to the Office for National Statistics (ONS):

The top 10 nationalities in order are Romanian (by far the largest), Polish (the next large number), then Italian, Bulgarian, Spanish, Portuguese, french, Irish, Lithuanian and Greek.

For the first time ever, the ONS has broken down exactly who is leaving Britain by age, revealing how Britain’s already ageing society is losing young people while drawing back the elderly.

Below are the net migration numbers for Brits according to the ONS, as featured in the Telegraph.

And here’s the shocker:

👉🏽 According to the ONS, “around three-quarters of British nationals who emigrated in the YE June 2025 were under the age of 35.”

👉🏽 net of 110,000 young Brits left in one year.

This means the UK isn’t just losing people.

It’s losing the future — its workers, innovators and entrepreneurs, and taxpayers.

Much of this pain comes from long-standing structural issues such as a:

Much of this pain comes from long-standing structural issues such as a:

- Weak job market

- Stagnant wages

- High housing costs

- Rising employer costs under previous governments

Although the recent Labour Budget will most likely accelerate the number of young people leaving the UK, this isn’t a one-party issue. It’s a systemic one.

👉🏽 Meanwhile, older Britons are returning or not leaving. Net migration for

➝35 to 44 year olds was only -15,000

➝45 to 54 year olds, it was only -2,000

➝55 to 64 year olds, 7,000 more people actually moved back to the than left.

➝Over 65s, 11,000 more people moved back to the UK than left.

The 35 to 54-year-olds are likely already tied down with:

- Marriages or being in a relationship where one person might want to move and the other in unsure.

- responsibilities of raising children and their education (which they’d have to pay for if they moved abroad but they might get for free here in the UK),

- mortgages (which have a psychological burden),

- careers (which would be harder to start again in another country) and

- Extended Family and ageing parents.

Meanwhile, the over 55s who are returning more to the UK than they’re leaving are likely doing it because:

- They’ve already had their fun and seen the world

- They might miss family and friends

- They might need the NHS more as they get older

- They likely want access to their state pensions.

Part 2 – The Five Forces Pushing Young People Out

Here are 5 reasons why young people are leaving the UK:

1. Stealth Taxes Eating Into Take-Home Pay

Frozen thresholds mean millions pay more tax without ever getting richer.

The Office for Budget Responsibility (OBR) says there will be:

- 5.2m new taxpayers

- 4.8m dragged into 40%

- 600k dragged into 45%

This has been building for years.

By 2030, almost 20% (1 in 5) employees will become higher-rate taxpayers compared to 8% in 2021 when the thresholds were frozen.

Plus, Student Loan Threshold Freeze = More Repayments, Sooner

Graduates start paying back earlier, even as wages stagnate.

This functions like another stealth tax.

2. Employers are Hiring Fewer Young People

From October 2024, employers’ National Insurance rose, and hiring slowed.

Graduates and school leavers were hit first.

Youth unemployment is now 15%, the highest in a decade outside the pandemic.

Over 700,000 young people are out of work.

3. Housing Costs Have Become Absurd

40–60% of income is spent on rent in major UK cities.

Then add food, utilities, transport, council tax…

Young people feel “stuck” before they’ve even started.

4. Cold Weather, Higher Crime and Rising Racism

These all speak to an environment that a lot of people don’t like.

The cold weather is balanced out by increasingly hotter Summers and we personally like to break up the winters with some time outside the UK somewhere warm, while also looking for small ways to appreciate and enjoy the changing seasons.

However, the higher crime and increasingly hostile environment are of great concern, and it’s clear why this is forcing people to move to other countries where they might feel more accepted.

That said, the grass is not always greener.

Take the weather, I was speaking to someone yesterday whose sibling recently moved to Australia, and she said that parts of Australia have a thin Ozone layer, meaning they have little protection from the Sun and a higher risk of skin cancers.

5. Global Mobility Has Shifted — Young People Are Leaving Because They Can

Remote working. Fast wifi. Easy video calls. Cheap European flights. English is a global business language.

The world has shrunk.

A young Brit today can build a life in Lisbon, work for a London startup, earn in pounds, operate entirely in English, and fly home in around two hours — something that simply wasn’t possible a generation ago.

Young people aren’t just being pushed out. They’re being pulled toward new possibilities.

Part 3 – Where They're Going and Why

There are many countries, but Australia stands out, especially for White Brits.

Working holiday visas for Brits rose 80% in a single year.

Youth unemployment is under 10%.

Wages are often higher.

But beyond Australia:

Portugal has digital nomad visas.

Spain and Germany offer remote work routes. My brother recently moved to Malaga in Spain and is loving it there.

We recently visited and couldn’t believe how good it was.

He pays 1500 Euros (£1300 a month), and for that he gets:

Warm weather all year round, 8 minutes walk to the beach, high-end 2-bedroom flat with 2 bathrooms, including a swimming pool, gym, jacuzzi, and co-working space, and the pace of life is slower, and people are really friendly. Really good vibes!

The UAE is also extremely popular and offers tax-free salaries. I’ll share more about the UAE in a minute.

Here is a table I found with the top 10 most popular destinations for Brits. Those destinations are:

Spain, United States, Australia, France (this was a surprise), Italy, Germany, United Arab Emirates, New Zealand, Ireland and Canada.

Now, all that said, my lived experience as a Black person in the UK is that Black people are mostly looking at:

UAE (Dubai, Abu Dhabi and Sharjah are popular)

I have heard mixed stories about the UAE.

Some love it!

For example, 2 days ago, we met Jamelia, the award-winning singer, actress and television personality.

She moved to Dubai in 2024, and we asked her about her experiences, and she loves it there.

She moved because she wanted a different environment.

One tip she gave was that she worked for a whole year, saved up lots of cash and then moved.

We’ve previously done interviews with BrickzWithTipz (Dubai) and Dr Amina Yonis (Sharjah, which is cheaper), and they had very good things to say about the UAE.

Note that everyone I’ve spoken about so far is a public figure, so you might be wondering, what about everyday people?

I spoke with my friend (an Accountant) who moved there with all the perks before Dubai became very popular.

She lived and worked there for years, then got married, and they had 3 children.

However, recently, she moved back to the UK, and I asked why, and she said 2 main reasons.

- It got too expensive to pay for private schools for our children, so we moved back for the UK State School system.

- She moved back for the NHS, because paying for a family of 5 out there got too expensive.

Plus, all those perks she had for moving there had dried up because there are now too many people moving there, and they don’t need to offer those perks.

From other people, I’ve also heard that Dubai is very expensive and that people have a good lifestyle there, but at a cost.

They never save any money there at all.

Some reliable sources living there now have said that Abu Dhabi is better than Dubai for families.

What do you guys think about this? What’s your personal experience? What have you heard from others?

Comment below and share.

Anyway, back to the list of places I’ve seen Black people move to (as well as Asians, Whites, etc), they are:

- UAE

- Qatar

- Canada (a lot of NHS doctors move here)

- Portugal

- Bermuda (high-income area but high cost, too)

- African countries like Ghana (quite a few of our friends have moved here), Rwanda, Kenya, Nigeria, South Africa, Gambia, and Tanzania.

- Caribbean countries like Barbados, Grenada (we met a 37-year-old yesterday moving there), Jamaica, and St Lucia.

- Asian countries like Singapore (we visited and loved it, and two of our friends moved here), Malaysia, and Thailand.

Jump in the comments and let me know what countries you’ve seen friends and family move to if they left the UK

Part 4 – But There's a Deeper Story – A National Mood Shift

Let me know if this resonates with you… In the UK, there is a growing sense of drift.

A feeling that the UK has lost its spark and there is a cloud of negativity amplified by social media

Young people are losing belief that the country offers opportunities.

This is not just economic. It’s emotional, psychological, and cultural.

When a generation stops believing in its own country, migration simply accelerates.

Part 5: Why Older People Return and Why That Matters

Over-35s are:

- Less likely to leave

- More likely to return

- More rooted

- More attached to community, family, stability

- Thinking about children, careers, and belonging

- Thinking about their health (NHS) and their pensions.

Modern communication also makes returning easier.

This generational contrast shows something important:

Freedom drives you out, Stability pulls you home. Your twenties are about exploration. Your thirties and forties and beyond are typically about being rooted.

This helps explain the earlier migration curve.

Part 6 – Before Leaving the UK – The Catastrophic Risks You Must Understand.

Here’s the part nobody talks about.

Leaving the UK can be a smart move.

But for many people…

…it can also be catastrophic ⚠️ . Here are some reasons:

1. Working Abroad Without the Right Visa Can Destroy Your Future

Immigration lawyers warn that this is exploding.

You could face:

- Fines

- Deportation

- Tax penalties

- Future visa bans

Remote work ≠ permission to work.

2. Lower Living Costs Abroad Often Come With Lower Salaries

Cheaper rent means nothing if:

- Your income drops

- Career progression slows

- You lack professional recognition

People often underestimate that in many industries — healthcare, law, finance, engineering, teaching — your UK qualifications don’t automatically transfer abroad.

That means you might not be allowed to work in the job you trained for, or you might have to start again, sit new exams, or accept a lower role.

This can set your career — and your finances — back by years.

3. You Lose the Financial Safety Nets You Understand

The UK has:

- A generous tax-free ISA of £20k a year per person. So £40k a year for couples. Very few countries beat the UK’s ISA system. Just think about that.

- The NHS, although far from perfect.

- Strong worker protections

- Predictable pensions (although the goal post keeps moving, which you also see in other countries)

- Tax rules you can follow (though not always easy)

- The state school system.

Some countries have none of this, or they’re of very poor quality, or you need to pay a lot for them, such that it wipes out some of the benefits of moving.

You might not feel the pain for a year, but you will over a decade.

4. Emotional Wealth Matters

Family, friendships, belonging, support systems, these are invisible wealth. You don’t realise how valuable they are until they’re gone.

5. You Can End Up In Jail

Popular countries in the Middle East offer sunshine, higher salaries, and a tax-free lifestyle, and that pulls in thousands of young Brits every year.

But what people don’t always realise is this:

👉🏽 The laws in the Middle East are very different from UK laws,

👉🏽 They are strictly enforced,

👉🏽 And breaking them — even unintentionally — can lead to arrest, detention, or deportation.

For example, in countries of these countries:

- Public behaviour rules are much stricter

- Alcohol laws vary

- Cohabitation rules can apply

- Social media posts can be criminalised

- Late payments or unpaid debts can be treated as criminal offences, not civil ones

- And working without the correct visa is taken extremely seriously

In the UK, missing a payment might lead to a letter.

However, in the middle East, for example, it can and does lead to criminal charges.

This means that young Brits who move there without fully understanding the legal system can find themselves in very serious trouble very quickly.

Migration advisers say:

“The biggest problem is people assuming UK norms apply abroad. In some Middle Eastern countries, they don’t — and the consequences can be severe.”

So the message is simple:

You must understand the legal system of the country you’re moving to — especially if it’s not aligned with Western norms.

Because a move meant to improve your finances can end up threatening your freedom if you don’t know the rules.

Part 7 – So Should You Leave The UK? (Biblical Perspective)

The real question is…

Are you leaving to escape? Or leaving to pursue something?

You know, whenever people talk about leaving the UK today — whether it’s because of the economy, the cost of living, or just feeling stuck — I’m reminded of two powerful stories in the Bible.

And they teach something essential about big life decisions like migration.

Story 1: Isaac — He Had The Call to Stay

In Genesis 26, there was a severe famine in the land.

The modern-day equivalent of economic pressure, cost of living crisis, lack of opportunity and so on.

People were moving.

Opportunities were drying up.

And Isaac was preparing to leave for Egypt — the place everyone believed had better prospects.

But then something unusual happens.

In Genesis 26:2–3:

2 The Lord appeared to Isaac and said, “Do not go down to Egypt; live in the land where I tell you to live.

3 Stay in this land for a while, and I will be with you and will bless you. For to you and your descendants I will give all these lands and will confirm the oath I swore to your father Abraham.

Isaac listens. He stays.

And in the same year — while everyone else is fleeing — he prospers a hundredfold.

Genesis 26:12-13 says:

12 Isaac planted crops in that land and the same year reaped a hundredfold, because the Lord blessed him. 13 The man became rich, and his wealth continued to grow until he became very wealthy.

“Planted crops could mean that he invested in the land”

Sometimes the right move… is not to move at all. Not because the situation isn’t hard, but because your purpose for that season is in the place you’re tempted to run from.

Story 2: Jacob — He Had The Call to Go

Fast forward to Genesis 46. Jacob is older.

A door opens for him to relocate to Egypt — a completely different culture, a new economic system, a fresh start for his whole family.

But Jacob isn’t sure, and here is the key bit…

He pauses in Beersheba to seek God before taking such a big step.

And God said to him in a vision at night:

“Do not be afraid to go down to Egypt… I will go with you.” (Genesis 46:2–4)

3 “I am God, the God of your father,” he said. “Do not be afraid to go down to Egypt, for I will make you into a great nation there. 4 I will go down to Egypt with you, and I will surely bring you back again.

And that move becomes the turning point for an entire nation.

Sometimes the right move… is to go.

Not out of fear, but because your next chapter is tied to a new environment.

The lesson from both stories is this:

There isn’t a “holy answer” of always staying… or always leaving.

Isaac was blessed by staying.

Jacob was blessed by going.

The wisdom is in knowing which season you’re in.

And here’s the part most people miss:

There’s a difference between a push-based migration and a purpose-based migration.

If you’re moving just because life is hard, that’s a push.

But if you’re moving because you’ve reflected, sought counsel, prayed, and genuinely feel led — that’s purpose.

And purpose always leads to provision.

So as you think about whether to leave the UK or stay, remember:

Some people are meant to stay and build.

Others are meant to go and grow.

The key is not the country — it’s the clarity.

Part 8 – How Young People Can Still Build Wealth In the UK and Similar Economies

Here’s how to build wealth even in a tough UK economy:

1. Build the 4 Pillars for building wealth

- Build the mindset

- Build the habits

- Build the system

- Build the life

These are the 4 pillars of our new book, The Wealth Habit, and we show you exactly how to do it.

This approach to building wealth is applicable no matter where you are in the world, and it will help to make wealth building effortless, inevitable and sustainable for life.

Order your copy of The Wealth Habit, and while you’re there, gift 🎁 a copy to a loved one.

2. Design your tax strategy intentionally

Use ISAs, pensions, salary sacrifice (while you still can), and side business structures.

3. Build global skills

Skills are mobile. Jobs aren’t.

4. Start investing early — even small amounts

Compounding is the great equaliser.

5. Focus on ownership, not just income

Income pays bills. Ownership builds freedom. The more global that ownership, the better.

Part 9 – Conclusion

The UK is changing. We’re entering a decade of higher taxes, low growth, low productivity and high cost of living.

Young people are responding by leaving. What will you do?

In case you’re wondering what we are doing, we still live in the UK, and our dream has always been to have a hybrid of living here while spending time in other countries (in Africa and beyond) during colder months.

This is something a lot of Brits already do and have done for decades in places like Spain, Portugal, etc.

👉🏽Whether you stay or go, you can still design a life of freedom if you approach it strategically, not emotionally.

Let me know in the comments:

Are you thinking about leaving the UK? And why? And where are you considering moving to? Comment and let me know.

If you found this helpful, share it on WhatsApp with someone weighing their options.

Don’t go anywhere—check out these resources on building wealth in difficult times:

- Book a Power Hour Financial Coaching Session

- 10 Silent Wealth Destroyers In Your 30s and 40s

- You're Trained To Be Poor (10 Shocking Money Traps)

Watch the video version of the real reason young people are leaving the UK:

As always, in all things, be thankful and seek joy!

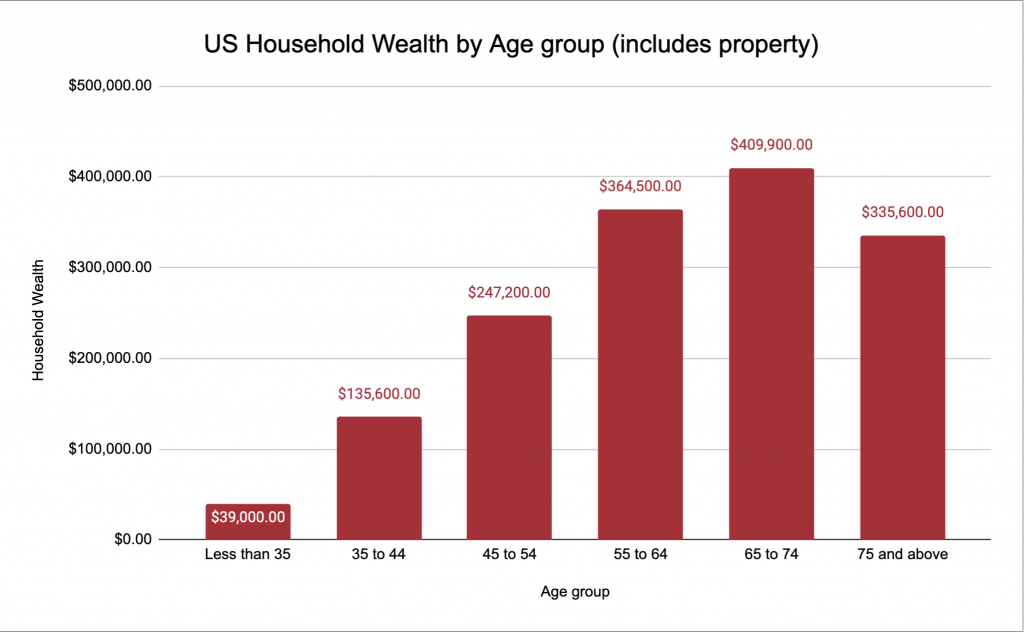

Pause for a moment and react in the comments. Does this surprise you?

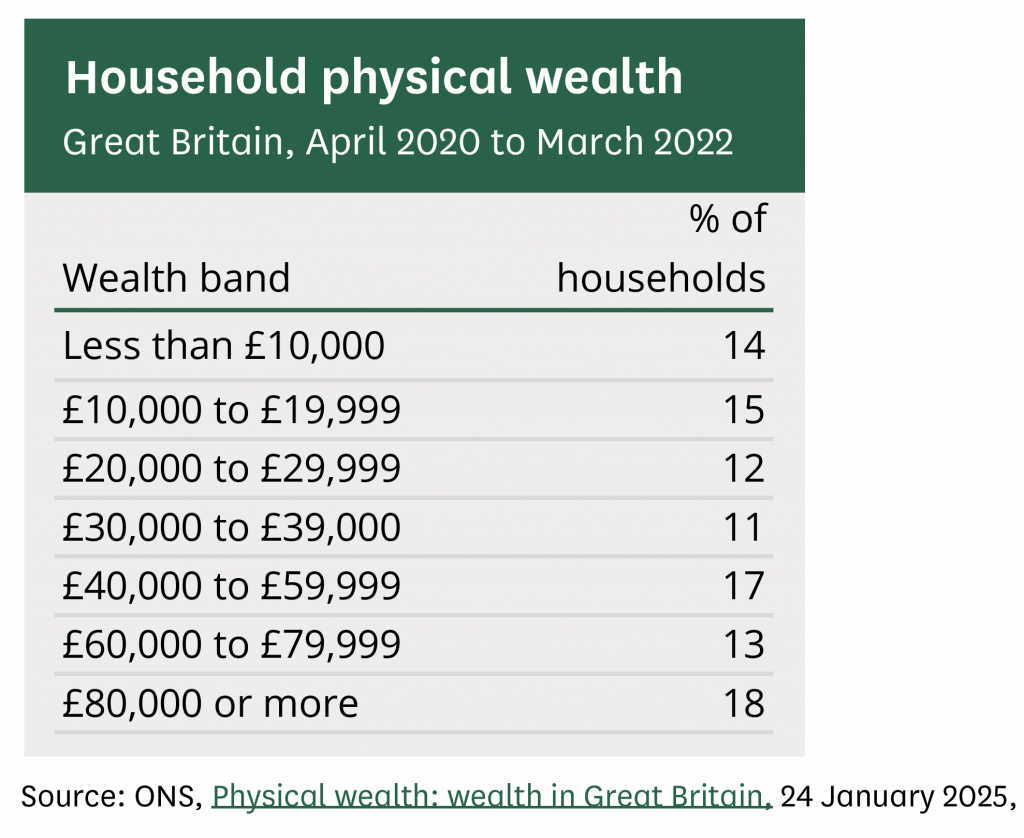

Pause for a moment and react in the comments. Does this surprise you? Reading the last paragraph might make you think, property is the most unequally distributed type of wealth in the UK, but it isn’t.

Reading the last paragraph might make you think, property is the most unequally distributed type of wealth in the UK, but it isn’t.

The key difference is that:

The key difference is that: